We independently assess all our recommendations. Purchases through our links may earn us a commission.

We independently assess all our recommendations. Purchases through our links may earn us a commission.

A Guide on All Matters Related to Short Selling for Readers Looking to Understand What Is Really Going on in the $GME Saga.

A group of small investors on Reddit rallied around the heavily shorted GameStop.

In a price explosion of epic proportions that no one this side of Wall Street understands yet, the $GME stock price shot upwards of $400, peaking on January 28.

That meant billions in losses for the short selling hedge funds.

The online trading platform, Robinhood, where most of those Redditors trade, temporarily stopped trading of $GME.

Prices fell back sharply but still remain quite high, certainly not back down to the near-zeros where the short sellers had driven them until late last year.

However, now those small investors who bought when the stock was very high are losing money.

Much hue and cry was raised over all this price volatility, the losses and the actions of Redditors and Robinhood.

There was a Congressional hearing, but it didn’t lead to much consequence for anyone.

Since Robinhood had to remove its trading ban in a few days, the stock went high again, but in a slow and steady surge. It’s been hovering around the $200 mark for one month now.

The $GME phenomenon is not going away. And yet, we have not seen any efforts from anyone mainstream – the journalists, the finance professionals with access to Big Media, or any government body – to fully expose the underlying mechanics of exactly what happened and how.

The casual observers, whether they would like to wet their toes in the arena of small trading or wish to develop a more informed opinion of the events, have nowhere to go. No one has focused on the problematic short selling of $GME, driving its price to near-zero despite the fact that the company has almost no risk of going bankrupt in the near future. The positive role of recent management and strategy changes are also typically ignored in recent analyses as the saga continues.

The spiking up of $GME stock prices involved financial processes with such names that range from dry finance to a touch of the sci-fi: gamma squeeze, call options, diamond hands, and short squeeze, to name a few.

You are correct, however, if you thought that the whole thing begins and ends with short selling somehow. While we intend to analyze the GameStop saga from the beginning to its current status in future articles, it would be impossible for the general reader to dive into it without understanding short selling first. So, here are a few things you absolutely must understand about short selling.

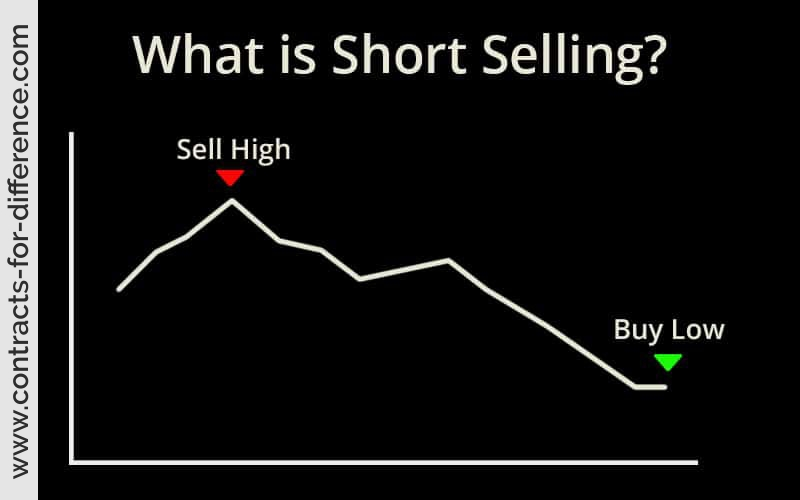

To Short or Not To Short?

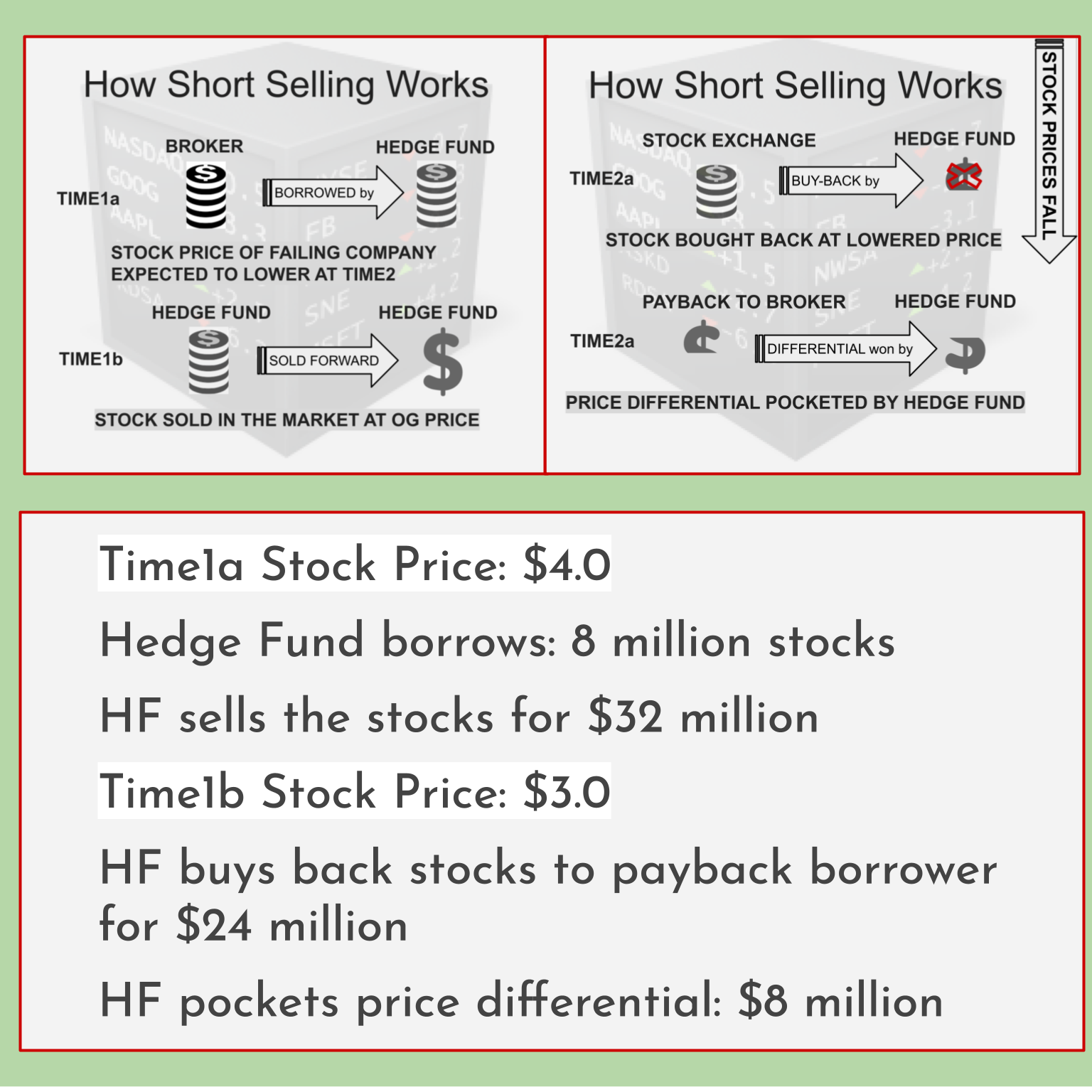

Short selling has always been controversial by default since it profits from the failure of other businesses. Here is how it’s done:

a) Hedge funds are big investment firms that engage in high-risk trading, often probing markets for businesses doing poorly.

b) Predicting stock prices of such companies to go down, they borrow stocks from big lending institutions.

c) They sell these “borrowed” stocks in the market and wait until the prices go down. (In contrast, regular buyers of stocks expect to profit when prices go up. Their positions are called “long”.)

d) The key dynamic here is the obligation to return the borrowed stocks to the lender in due time. By then, the stock price is usually lower, as predicted.

e) Now, the hedge fund can buy the same number of stocks they had initially sold, at lower prices.

After the stocks are returned to the lenders, the hedge fund gets to pocket the price differential, as the figure below illustrates:

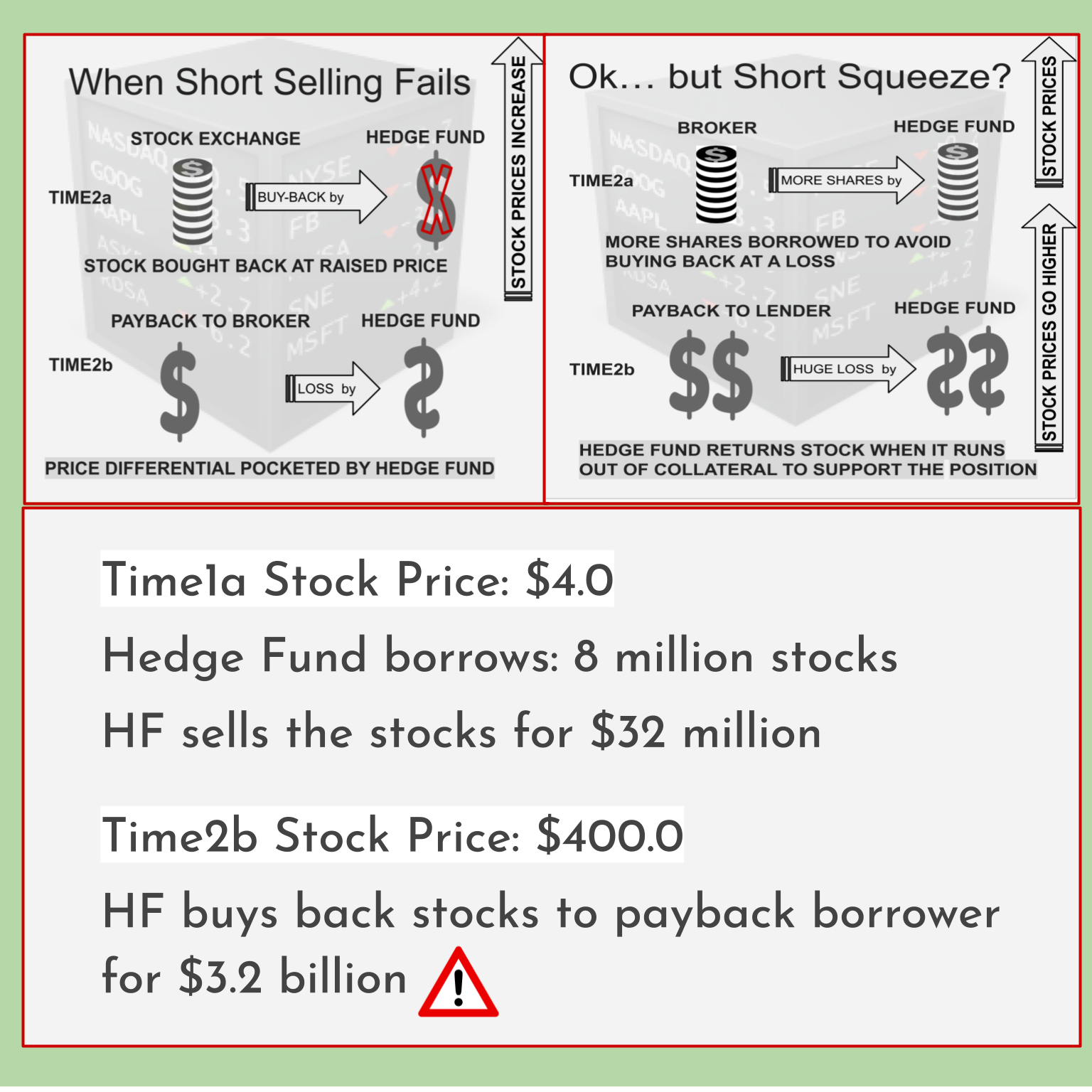

What happens when short selling fails? If other factors combine to increase, rather than decrease, the stock price of the company, the short sellers will have to buy back the stocks at a loss in order to pay back their lenders. However, what typically happens is that hedge funds borrow more stocks to “cover their short positions”, as they call it. They sell these forward too in the hope that their price-reduction predictions would be met.

A key role is that of the lenders who are making money by exacting very high interest rates on the collateral. Collateral is the term for the money a hedge fund must deposit with the lending institution when borrowing stocks. Thus lenders are happy to keep lending out shares despite the stock price going up.

A “short squeeze” occurs when the prices go so high that the hedge fund runs out of money to deposit as collateral to keep “covering their positions”. Note that collaterals (and the accompanying interest margin) will also be much higher for rising stocks. This forces the hedge fund to close its short position by buying back shares and paying back lenders at a huge loss to the fund. The losses that the hedge funds reported after 27th January, the peak of the $GME saga, were in the billions.

Most people have wrongly assumed that the short squeeze is the only reason for the extreme spike that was seen in January and have blamed r/WallStreetBets (the Reddit thread responsible) for it. However, there were far more factors involved. As promised, our next piece on GameStop will expand upon those factors for the casual reader.

For now, back to short selling.

Do-gooders or the Merchants of Venice?

One assumption that stands out in the media and the statements from the finance world is that short sellers serve an important function in the stock market, that they perform in-depth research to expose problems in companies, helping to bring stock prices lower to where they should be. But if that is indeed the case, why has short selling always been controversial and what are its limits – the situations where the benefits of short selling may not apply?

Short selling has been around since the days of the Dutch East India Company in the 17th century. It was formally banned in Europe and the United States for the most part of history. However, regulations were poorly enforced, allowing traders to work through loopholes.

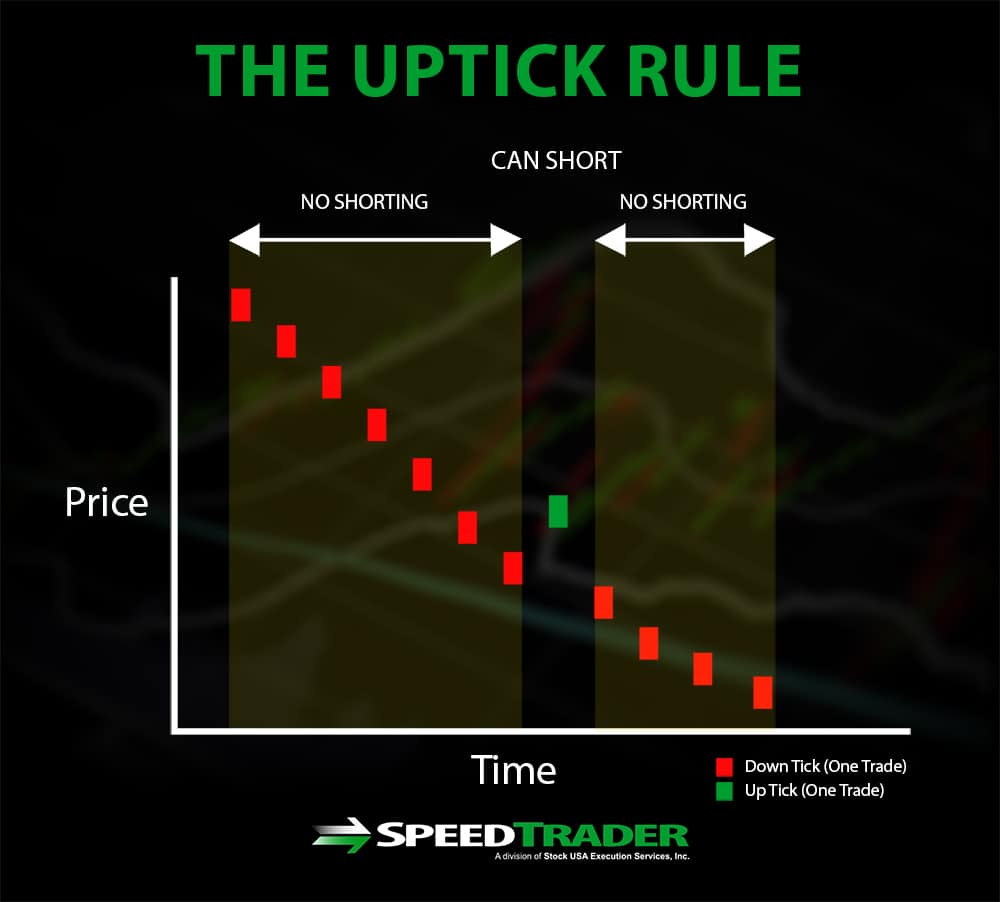

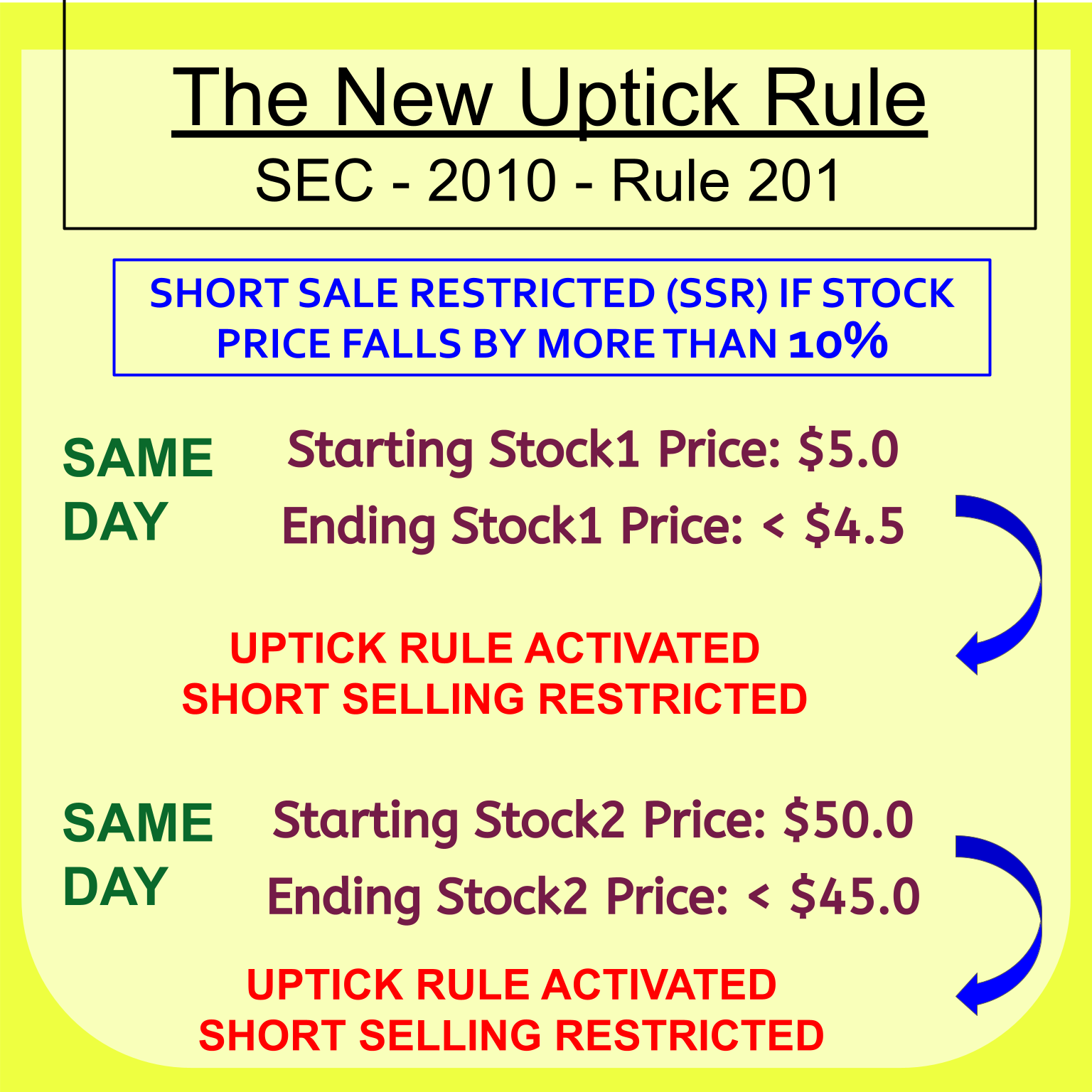

When England abandoned the gold standard in the 1930s, the New York Stock Exchange formed the Securities and Exchange Commission. The SEC adopted Rule 10a-1 to address concerns about short selling. Nicknamed the “uptick rule”, it prohibited shorting of stocks during price declines. The trading of phantom shares, called “naked short selling“, was also banned. Both these rules were a safeguard against price manipulation and against depriving sincere long-term investors of purchasing stocks.

The crash of 2007-2008 revived the controversy when a bunch of foreseeing investors profited by shorting the mortgage market. But the SEC had already lifted the uptick rule in 2005 in a pilot program to find out if it made any real difference in the stock exchange. It was dismissed for good after a technical report commissioned by various international investment associations revealed that short selling bans did not prevent market volatility.

Thus, the traditional failures in enforcing SEC regulations were now touted as “proof” that short selling bans were not needed!

In 2010, the SEC seemed to realize its cheekiness and announced the new Rule 201: If a stock’s price falls by more than 10% in a single day, the uptick rule would then apply. That is, prices would first have to show upward movement for any further shorting to be legal.

Excuse me, your Shorts are too Short… The Moral Debate

Short selling counts on failures of businesses. It can turn the efforts of any startup company to get its stock a respectable price valuation into an uphill or even a losing battle. In their Q&A style piece, this online trading guide sums up the financing problems companies face when their stock declines:

“In practice, share prices do matter and … a loss of confidence when they fall can be extremely damaging – as we have seen in banking. [M]any companies have loans and warrants which are secured against shares: so if the price drops, there is an immediate risk that loans can be called in, and a longer-term cost in raising finance. In a credit crunch, companies with a volatile share price, or a low one that represents a weak asset base, will be unable to raise money at all. Worse, companies in the financial sector may have statutory capital adequacy requirements which count their share capital as part of the ‘permanent capital’ of the company. So a company can run into serious financial and regulatory difficulties i[f] the share price falls. Plus, of course, they will become a takeover target.”

Turn to the suits or the professors and they would explain this and all other criticisms of short selling:

Q. Short sellers can distort or exaggerate a company’s weaknesses to short it…

A. Criminal or shady intentions are possible in every economic activity.

Q. Lowering prices means the small investors lose their investments…

A. That’s why prices need to be low for poor or fraudulent companies, so small investors don’t suffer.

Q. But what if short sellers gang up on a stock unfairly depressing the prices for profit?

A. Won’t work. Prices will balance when short sellers buy back shares to pay off the lending institutions. Also, remember how SEC rules ensure shorting will be lower when prices are going down?

Q. But short sellers often also buy additional shares of the same company in the regular way (called ‘going long’) which means they also have voting rights in the corporate elections for the same company that they are shorting. Isn’t that a conflict of interest?

A. Agree on this one. There needs to be better regulation to separate voting rights from short sellers’ activities.

Q. And how about the ‘lending of shares’? Lending institutions have these shares via their users (i.e. small investors) purchasing ‘long’ shares in the company. Loaning these to hedge funds who will ‘sell’ them to other buyers in the market would deprive original investors of their voting rights, no?

A. Benefits trickle down in other ways to those small retailers. Plus, there is usually no way of knowing whose shares have been shorted, so voting rights should not be affected in practice. By the way, we basically answered this question in answer to the last one.

Q. Did you? My last question basically described naked short selling, which was banned you said. How can short sellers borrow and sell forward shares which have already been purchased by the ‘long’ investors? And how come short sellers kept shorting $GME even when its stock price was approaching zero last year?

A. Look, you have dug in this far and that’s pretty courageous of you. Big Money is at stake here and short sellers have revealed fraud in plenty of scenarios they have shorted. To fully understand, you need to dig even deeper than your ability to handle the truth. So, maybe go back to your puny jobs?

So, a capitalist system largely favors and even encourages short selling of companies. What little regulation exists is barely enforced and no one minds. It’s true that research in finance has mostly yielded favorable results of short selling, but all that research was done on large trends in the market under regular circumstances. What about companies who may be simply going through a rough patch, the start-up spurts, training wheels, or may be – like GameStop – in a messy process of cleaning up their act and turning things around?

For instance, short selling activity against a company increases when:

- the company initially opens up its stock to the public and the offering is deliberately low-priced to attract buyers.

- during important mergers.

Neither mergers nor going public have anything to do with fraudulent or other poor performance indicators that short sellers are touted as being vigilant about. The magical assumption seems to be that short sellers would simply never engage in manipulative price-depressing. So what happens when short sellers do not observe the supposedly self-initiated ethics?

Instead of studying short selling the usual way, a North American team of professors in business economics focused on days where prices had declined sharply. They made sure to study only irregular declines, that is, when no problematic news on the company had come out. They found evidence of aggressive short selling activity on all such stocks. The more aggressive the shorting, the steeper the decline in the price. Short sellers were able to circumvent Rule 201 by either going to institutions that do not observe it, or by using temporary up-bidding quotes.

Another study by a professor of finance differentiated between informed and contrarian short sellers. While the informed short sellers were able to read the temporary mispricing of stocks, the contrarian short sellers did not. These latter, less informed short sellers tend to short stocks that are temporarily undervalued but are winning stocks by other criteria. In all likelihood, they are simply going through a downward swing on an overall upward course.

Now, name one stock which could have been going on a temporary downswing, helped along by the pandemic (where nearly every non-mega business suffered losses), and which the short sellers kept shorting heavily even when stock price dipped under $5.00?

I’m pretty sure your answer is GameStop.

Bear Swipe or Bull Pull?

In contrast to the bearish tactics of short sellers, several bullish positions on GameStop nursed the stock as deep-value investors since 2019. These include Michael Burry, Ryan Cohen, Keith Gill of Roaring Kitty, and several degree-holding investors with pro-$GME essays on Seeking Alpha going back a year. Not only did they help keep the prices above zero, their enthusiasm and belief is what attracted the attention of Keith Gill and r/WallStreetBets and helped bring the company in the very favorable position it is today.

All of these people are professionals in various capacities and at least two, Burry and Cohen, have done great in the world of business and finance. All these people seem to have recognized early on that the GameStop stock was unfairly undervalued due to heavy short selling and had upswing potential. But you will not find much reference to these valid bullish positions on any mainstream writing out there.

It is the hope of this author that this review of short selling has raised many healthy and constructive questions in the readers’ minds about how the whole stock-trading system works and why its many cracks allow the “rich to get richer” and “underperformers to fall further”.

In future articles, we intend to address all these questions and answer them. If the world of finance needs to democratize, greater sharing of buried information on topics affecting our economy must be the first step.